How to Decarbonize Cement Industry?

This paper would not have been possible without the support of my colleague, Hafizhul Aziz from Semen Gresik.

Cement is the building block of our infrastructure. It is a substance used for construction that harden and bind other materials together. Mixed with sand and gravel, it produces concrete. Concrete is the most widely used / most consumed material in the world, just behind only to water.

But did you know that cement production is also the source of enormous GHG emission to the atmosphere?

Emission of Cement Industry

Cement is one of the most polluting sector on the planet. According to US Geological Survey, global cement production is 4.4 billion tonnes in 2021. As you may guess, it grows exponentially, follows the fast economic growth and its subsequent building construction. Consequently, cement sector alone emits 1.5 billion tonnes CO2eq in the atmosphere (refers to 2016 data, it varies depending on source, but still, the magnitude can’t be ignored), thus contributing to approximately 3% of global GHG emission (Our World in Data, 2016) .

For a comparison, cement industry’s emission is much larger than emission from aviation or shipping industry that shape the 21st century globalization by transporting people and goods across the world!

Why Such Enormous Emission?

Economic growth is the strongest driver of the large sum of cement footprint. In any place where economy is booming, building and infrastructure are developed very rapidly. China is a notable example. City of Shenzhen was just a fishing town in 1980 with population of 30,000 people (World Cities Culture Forum, 2022). It experienced a massive development and urbanization that converts the plain land into one of the largest megapolitan with a population larger than New York city. Now, imagine this pattern is replicated in all major cities in the developing countries. To give you a better perspective on the resulting cement consumption, take a look at the following chart.

Emission in Every Ounce of Cement

Before jumping into solution, it’s worth while to take a look where the emission is coming from in a cement production plant. Let me explain very briefly the process of making cement:

The raw materials are silica, magnesium, alumina and iron typically contained in limestone and clay that is mined from a quarry. Rocks are collected and transported, then crushed into smaller pieces. Pieces are then further milled as fine as powder. It is then going into heating process up to 1500 degree Celsius where the reaction happens (calcination) and release significant amount of emission. The resulting product is called clinker, which is then mixed with gypsum to finally become cement.

The energy used and CO2 emission corresponding to each process is summarized in following chart. In total, the production process release almost 1 kg of CO2 for each kg of cement. For your perspective, consider case of building a small house:

A very small 36 sqm house, where a family of four could live, requires 5 tons of cement. The resulting CO2 emission is 4.5 ton just to provide a simple shelter for that family.

How Can We Tackle It?

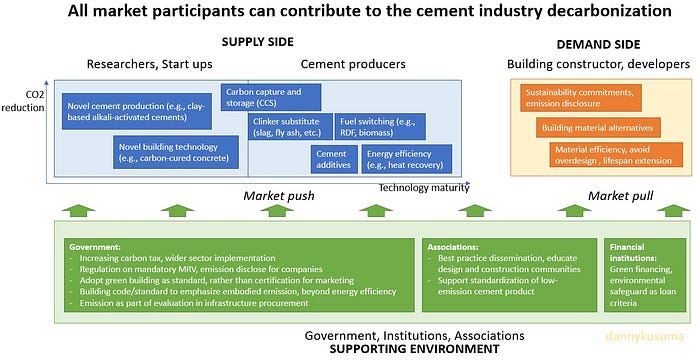

Now, let’s talk about the solution that we can do. Rather than blaming cement factories, I prefer a holistic approach which all market participants can contribute to promote decarbonization of cement industry (and building sector in general). Therefore, I propose a concept where it includes

1) supply side where cement factories can improve their production process,

2) demand side where construction companies as users play important role to “ask for” more environmentally friendly cement product,

3) also research community where innovation comes from, and finally

4) the industry environment which needs to be shaped so that it providea incentive and obligation, “carrot and stick”, for each market participant to contribute in lowering emission of the industry.

Cutting Emission in Cement Production

Strategy #1 Energy Efficiency

Cement production is an energy intensive process. Energy efficiency measures are obvious approach to reduce associated emission of cement production. Beside cutting down emissions, energy efficiency brings additional benefit to manufactures, which is making their product more cost competitive.

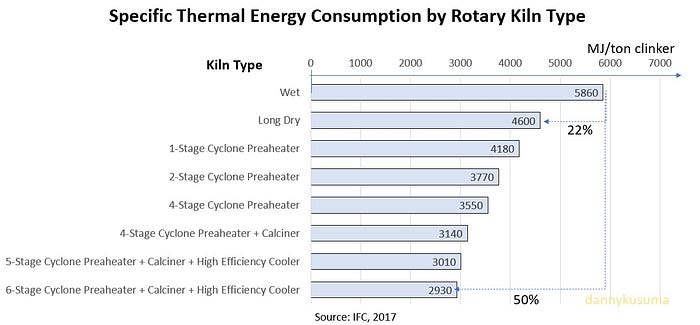

Know-how and reference are nowdays easily accessed. Energy efficiency best practices for cement plant and the associated investment cost are published by several institutions (European Commission JRC, 2010; European Commission JRC, 2013; US EPA, 2014; IFC, 2017a). The measures can be applied along the production line, from crusher, mill (i.e., high pressure roller mill), heat recovery (i.e., ORC turbine), preheating (i.e., cyclone preheater tower), and kiln (i.e., automatic conduction system) (Cantini, 2021).

Currently, the global average of cement energy consumption is 3.5 GJ/ton clinker and 109 kWh/ton cement. Manufacturers can apply Best Available Technology (BAT) that offers lower thermal energy and electricity consumption, 2.9 GJ/ton and 56 kWh/ton, respectively (UNIDO, 2014). Unfortunately, cement is a mature industry; there is no breakthrough technologies that are expected to significantly reduce thermal energy consumption.

Strategy #2 Clinker Reduction and Alternatives

Clinker production is the most energy-intensive, thus the most CO2-emitting process in the cement making. On average, 81% of cement consist of clinker, while the rest are a combination of gypsum and additives. Therefore, one of the way to reduce energy and emission is to mix cement with increased amount of alternative (non-clinker) material. The options are volcanic ash, granulated blast furnace slag from iron production, or fly ash from coal-fired power generation (UN CTCN, 2022a). However, supply of such materials could be limited and varies region-by-region. Moreover, it would be less available in the future as the steel and coal industry are also decarbonizing.

In the long term, development of Alternative Clinker Technologies (ACTs) that emits lower emission than ordinary Portland cement (OPC) could be more strategic approach. ACTs shall present similar performance to OPC; the most critical properties are mechanical performance , rheological performance, reduced chemical shrinkage, and chemical stability (Antunes, 2021). Several ACTs and the potential emission reduction are presented in the following chart.

Strategy #3 Fuel Switching

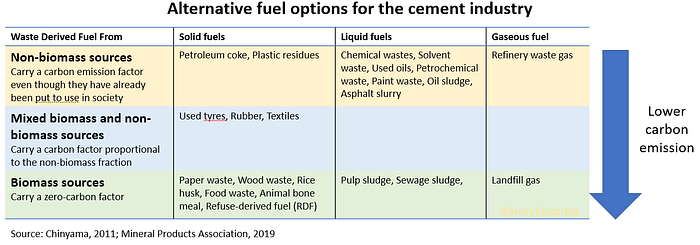

Usage of alternative fuels is already common in cement industry, and it has the potential to reduce emission. In the past, the primary goal was economic competitiveness as fuel accounts for a third of clinker production cost, while environmental benefit was considered as a side advantage. Additionally, alternative fuel from waste material contains additional mineral and metal that offset the use of virgin raw material, thus having a co-benefit of recycling.

Cement manufacturing is not picky about the type of fuel. A wide range of low-grade and waste derived fuels can be utilized as shown in the table below. The favorable conditions inside kiln system enables the use of alternative fuels. Kiln conditions of high temperatures, long residence times, an oxidizing atmosphere, alkaline environment, ash retention in clinker, and high thermal inertia, ensure destruction of organic material and trapping inorganic material (e.g., heavy metals) in the product (Chinyama, 2011).

There could be technical constraints that limit the use of alternative fuels. These include changed flame formation, altered cement chemistry and built-up/blockages which may require major equipment retrofits (Pnumat.com, 2021). Besides technical considerations, alternative fuels involve new supply chain where supply sustainability and quality could be uncertain. A solid business model is one of success criteria in such project (IFC, 2017b).

Biomass is an attractive fuel that offer net zero carbon emission. However, manufacturers needs to consider key issue of biomass around securing long term sustainable supply. Increasing use of biomass may require the use of virgin biomass where sourcing sustainability must be thoroughly checked (Mineral Products Association, 2019).

Besides the usage of waste material as alternative fuel, other approaches are being researched. Thermal plasma torch (electrification) allows the use of renewable electricity. Additionally, hydrogen is also proposed as fuel for cement production.

Strategy #4 Carbon Capture and Storage (CCS)

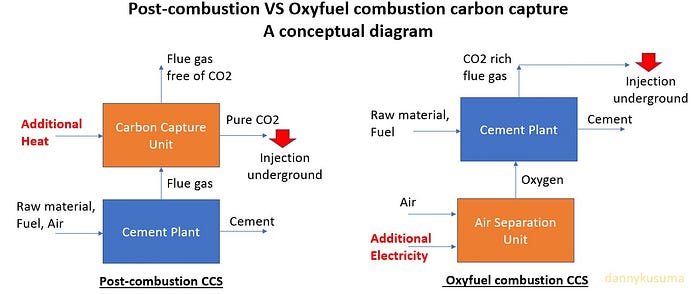

Strategy #1 to #3 won’t bring to net zero cement. No matter how efficient the plant or how green is the fuel, as long as the chemical reaction of the raw material generates CO2 (e.g., CaCO3 — > CaO + CO2), it is still not a zero-emission cement. This fact leads us to the last strategy, which is capturing the CO2 and injecting it underground forever, known as CCS. Research shows that CCS is one of the key to achieve net zero cement production (Fennel, 2021; McKinsey, 2020).

In general, there are two families of carbon capture technology that can applied for cement plant, post-combustion and oxy-fuel combustion (ECRA, 2012; IEAGHG, 2013). Post combustion CO2 capture involves installation of additional equipment to separate CO2 from the flue gas. On the other hand, oxyfuel combustion, as the name suggests, relies on the oxygen supply to sustain fuel combustion, instead of air. It results in CO2 rich flue gas which requires no / limited end-stage separation. CCS is an active research; to name a few, there are studies on technology readiness (Hills, 2015), carbon removal involving bioenergy with CCS (IEA, 2021), and techno-economic analysis of the CO2 chain (Jakobsen, 2016).

Since CCS involves CO2 transportation and underground storage, making it viable requires strong support from the government. It includes CO2 transport infrastructure, access to suitable storage site, legal framework, monitoring and verification and licensing procedures (UN CTCN, 2022b). Considering the necessary large upfront investment, project scale up and cooperation with other CO2 emitting industries would be necessary to allow economy of scale. Cement manufacturers are also needed to team up with players from oil and gas having expertise on CO2 injection underground.

Beyond Cement Manufacturers

As I briefly elaborated in the beginning, efforts from cement manufacturers alone could not solve the problem. Just simply imagine a case: a new cement product with zero emission is invented, but the project is abandoned since there is no construction company willing to pay premium price for that product. As you can see, price signal from demand side is equally important. Without real targets and real efforts from building constructors and developers towards net zero emission, cement industry decarbonization just won’t happen.

Government, associations and financial institutions also have essential role to shape the cement industry environment. Supporting the decarbonization, government could set higher carbon tax, mandate green building standard, regulate CO2 storage MRV, or even hold a construction tender that set usage of “low-emission” cement as a criteria. While associations could help disseminating best practices around the world to local players and bridging collaborating with academia. Finally, financial institution could simply stop financing construction project that is using high emission cement.

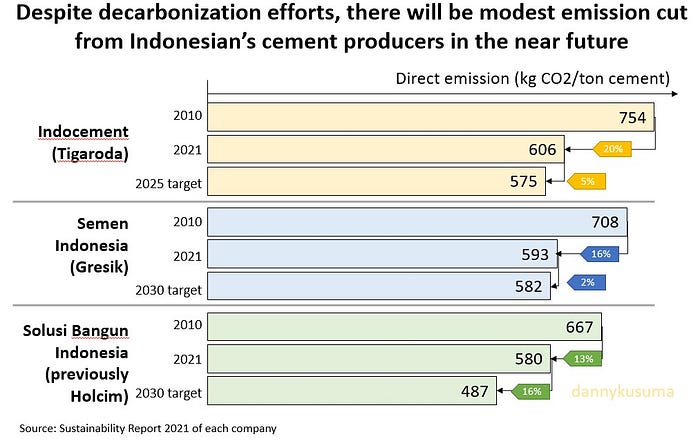

What about Indonesian Cement Companies?

As a final section, I would like to review on how Indonesian cement producers are performing in terms of lowering CO2 footprint of their products. Following chart is a short review of three companies who control more than 80% of Indonesian cement market share (Bisnis.com, 2018; Indocement, 2021; Semen Indonesia, 2021; Solusi Bangun Indonesia, 2021).

Indonesian manufacturers are currently trying to source alternative fuel for their plants, ranging from agriculture waste from farmers (republika.co.id, 2020) to RDF from municipal solid waste (sindonews.com, 2021). Morever, as also part to boost their image in the market, manufacturers are also pursuing “green label” certification (solopos.com, 2020).

Innovation Across the World

Indonesian cement manufacturers may not have a significant emission reduction in the near future, but I’m still optimistic especially when looking at what international players are currently working on.

Global Cement Magazine listed down innovations in cement industry across the world. I encourage readers to also take a look. Here are few of my favorite:

1) Cemex is researching on Vertua® concrete, claims to reduce 70% CO2 footprint;

2) Heliogen is developing high temperature furnace from solar heat;

3) DB Groups is starting to market CemFree, claims to reduce emission by 80%; and

4) CarbonCure who is making concrete that is able to absorb CO2.

Let us work together to decarbonize cement industry!